Introduction

If you’ve ever wondered “Is CreditVana legit?” or whether it truly offers free credit monitoring and scores, you’re not alone. In this CreditVana review, we dig deep into what this platform offers, how it performs, where it shines, and where it still faces uncertainty.

CreditVana brands itself as a free credit score and credit monitoring app that gives users daily updates, alert notifications, credit report card insights, and a marketplace of financial products — all powered by trusted credit bureau data. creditvana review

In this detailed review, we will examine:

- What is CreditVana, and how it works

- Its key features, strengths, and UX

- Mobile app performance and user feedback

- Credibility, data sources, and transparency

- Weaknesses, risks, and caution points

- Comparisons with competitors

- SEO / branding & marketing suggestions

- Final verdict and recommendations

By the end of this CreditVana review, you’ll have a clearer picture of whether it’s a tool worth trying or whether you should proceed with caution.

1. What Is CreditVana & How It Works

A. Overview & Positioning

CreditVana is a financial service app that provides users access to free credit scores, credit monitoring alerts, and personalized credit insights. It positions itself as a modern alternative to legacy credit reporting tools and “freemium” credit platforms that hide costs behind trial periods. creditvana review

Notably, it recently launched mobile versions (iOS and Android) that aim to deliver three-bureau credit reports — from Experian, Equifax, and TransUnion — to users without hidden fees or gimmicks. The company emphasizes it is “100% free” for checking the credit score itself.

Beyond credit scoring and monitoring, CreditVana review also has a marketplace of financial products (credit cards, personal loans, etc.), integrated with affiliate offers.

B. App Architecture & Underlying Data

According to its listing on Google Play, CreditVana review connects to a third-party provider, IDIQ, to access credit report and score data securely. The app also states that it does not issue loans itself — it displays offers from external lenders via affiliate partnerships.

Thus, the core value is in aggregation, visibility, alerts, and guidance — not direct lending. creditvana review

C. Enrollment, Identity Verification & Usage Flow

Users typically sign up with their personal information (name, address, date of birth, SSN or equivalent) to verify identity and link to their credit report. The app then retrieves (via IDIQ) a credit report and score, which is displayed in the dashboard.

Once enrolled, users can:

- View credit score & credit report card (factors affecting score)

- Receive daily monitoring alerts for changes (new inquiries, changes to accounts)

- Explore offers in a marketplace (credit cards, personal loans)

- Track credit over time via history charts or dashboards

The app also provides educational content and explanations to help users understand credit factors and how to improve their credit standing. creditvana review

2. Key Features & Strengths

This section highlights where CreditVana stands out — what it does well and the features likely to attract users.

A. Truly Free Credit Score & Monitoring

CreditVana review repeatedly emphasizes that checking your credit score is 100% free, with no hidden trial periods or forced upgrades.Many competing platforms lure users with “free trials” that convert to paid plans; CreditVana markets itself as avoiding that trap.

Daily refreshes and alerting cumulatively build value: users can spot suspicious activity quickly or monitor their credit changes in near real-time.

B. Three-Bureau Coverage & Aggregation

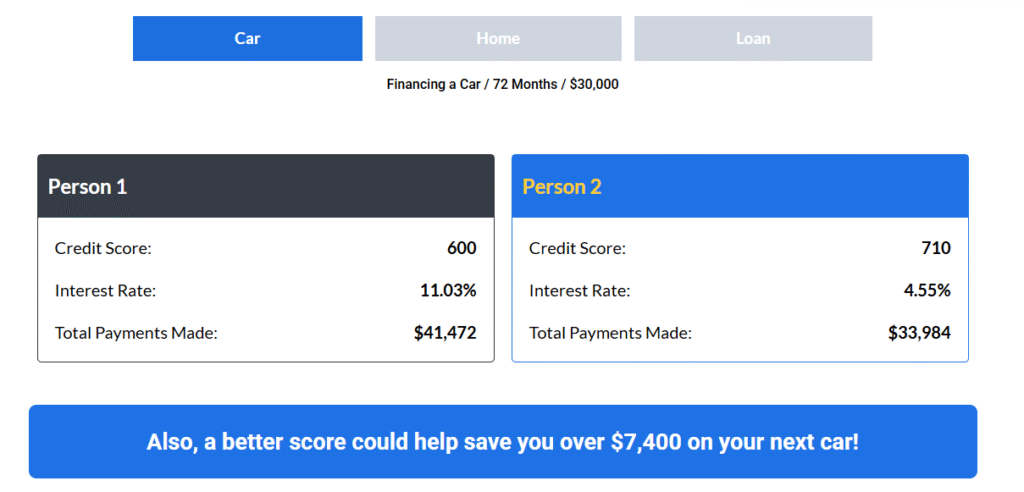

A strong selling point is that CreditVana review claims to provide credit data from all three major bureaus (Experian, TransUnion, Equifax) — a full panorama rather than partial. Many apps only cover one or two. This coverage enhances completeness and reduces “blind spots” in your credit profile.

Comparisons made in news coverage suggest that offering three-bureau data is one way CreditVana review is positioning itself ahead of traditional competitors. creditvana review

C. User-Friendly Interface & Mobile Experience

According to user reviews on iOS (App Store) and Android (Google Play), the app scores highly for ease of use, clean design, and intuitive workflows. The iOS version shows 5.0/5 (based on over 200+ ratings)

The Android version’s listing describes a simple dashboard, real-time updates, and affiliate offers with transparency.

This ease-of-access is critical: users want quick visibility into their credit, not complex navigation.

D. Alerts & Monitoring

CreditVana review provides real-time alerts of credit changes — such as new credit inquiries, account status changes, or unusual activity — which helps users detect errors or identity theft early.

Such monitoring is often the most valued feature among credit app users, because it affords peace of mind.

E. Marketplace Integration

Beyond monitoring, CreditVana surfaces relevant financial product offers (credit cards, loans) suited to the user’s credit profile. While it doesn’t issue loans itself, this affiliate marketplace can be convenient.

It means users can see options to expand or optimize their financial tools without leaving the app.

F. Educational Insights & Score Drivers

CreditVana review offers a “credit report card” — a breakdown of the factors affecting one’s credit score (payment history, utilization, inquiries, etc.). This helps users understand their weak points and take corrective action.

The app also periodically surfaces tips and suggestions to improve credit health.

3. Mobile App Performance & User Feedback

An app’s reputation ultimately depends on how real users perceive and use it. Here’s what the feedback and metrics suggest.

A. Ratings & Reviews (iOS & Android)

- On the App Store, CreditVana has a 5.0 rating (with 214+ ratings as of latest) — a strong positive sign.

- Many reviews praise its simplicity, “game-changing” free features, and ease of use.

- On Google Play, the listing notes that CreditVana connects securely to IDIQ for credit data, has a user-friendly dashboard, and offers in-app affiliate product offers.

Overall, user sentiment in public reviews leans positive, especially for core features like free credit access, UI, and lack of aggressive upsells.

B. Speed, Stability & Updates

The app recently updated to version 5.1.8 on iOS (Oct 2025), which suggests active maintenance and updates. Users mention occasional minor glitches or interface polishing needs, but nothing major in public reviews so far.

Given the sensitive nature of credit data, app stability, security, and latency are critical — early signs point to relatively clean execution.

C. Privacy, Security & Transparency

The app states that user data is encrypted in transit and shared only with IDIQ to fetch credit reports. It also discloses in the Play Store listing:

“Loan offers may include affiliate offers from licensed lenders … our data is encrypted … we do not sell your personal information or share it with advertisers.” creditvana review.

While these statements are standard and reassuring, real trust depends on rigorous audits and third-party verification — which is something users should monitor.

D. Monetization & Upsells

Though credit score checking is free, some features (e.g. accessing cash advances or certain premium features, according to some user-community commentary) are gated behind paid plans (e.g. “CreditVana Plus” or “CreditVana Builder”) or subscription fees. CreditVana Some user commentary warns that cashback / cash advance features are limited and require subscription. CreditVana review

Users reported that maximum advance amounts are small (e.g. $100) and that funds may take up to 4 days unless you pay a rush fee.

Thus, while the core app remains free, premium features or credit-advance services may have costs.

4. Credibility, Data Integrity & Transparency

Any credit reporting app must be held to high standards of reliability, trust, and legitimacy. Here’s how CreditVana stacks up in those dimensions.

A. Data Sources & Accuracy

CreditVana’s reliance on IDIQ as intermediary for credit bureau data is a standard approach in fintech — IDIQ aggregates and normalizes credit report data for apps.

The claim that CreditVana provides three-bureau data suggests a more robust and accurate view of credit than many apps which only access one bureau.

However, the app and media claims should be independently verified — e.g. comparing the app’s output with direct bureau reports — to confirm alignment.

B. Accreditation & Trust Seals

On the Better Business Bureau (BBB) site, CreditVana is not accredited. It also has had at least one complaint filed, which affects its BBB rating.

Lack of accreditation isn’t necessarily disqualifying, but it means users should be more cautious and scrutinize user feedback, terms, and privacy policies.

C. Transparency in Terms & Limitations

While CreditVana discloses that loan offers are from third-party lenders via affiliate relationships (not directly issued by CreditVana) on its Play Store listing, some deeper features (e.g. cash advance) have less visibility or clarity in their native site FAQs.

Some user commentary notes that FAQ, terms, and transparency for premium features are less robust than ideal compared to legacy banks or financial institutions. CreditVana

In sum, while the public-facing disclosures are decent, enhancing clarity around limitations, privacy, and premium tier features would strengthen trust.

D. Reputation & Media Coverage

Recent press from BIIA states CreditVana launched as a “premier free credit score app” with truly free access to three-bureau data, positioning it as a challenger to legacy platforms.

Additionally, there’s buzz that CreditVana is “surpassing Credit Karma” in accuracy or user sentiment. However, such claims must be taken with caution until backed by third-party metrics or audits.

Media coverage helps with brand awareness, but it is not a substitute for user reviews, security audits, and transparency.

5. Weaknesses, Risks & Areas for Improvement

No product is perfect. Here are some potential downsides, risks, and things to watch out for in CreditVana.

A. Premium Feature Costs & Upsell Friction

While credit score access is free, features like cash advances or advanced tools may require subscription fees (e.g. “CreditVana Plus”). CreditVana review This could disappoint users expecting a totally free service. The small advance limits and payment delays (or rush fees) may reduce perceived value. CreditVana review

Transparency around these tiers, fees, and limitations is essential to avoid claims of “bait-and-switch.”

B. Limitations of Data & Reporting Lag

Even with three-bureau data, credit reports are not instantaneous and may lag. Some user transactions (new credit, disputes) might take days or weeks to reflect. Users may misinterpret changes or assume accuracy that is partial.

Also, certain loan types, regional credit bureaus, or non-traditional credit sources may not be fully captured. The app’s ability to handle those edge cases depends on IDIQ’s integrations.

C. Privacy & Data Security Risks

Handling sensitive personal data (SSN, credit report, financial history) has inherent risks. Though the app says it encrypts data and limits sharing, any breach or misuse could be damaging.

Users should verify that the app has undergone independent security audits, encryption at rest/in transit, compliance with data protection laws (e.g. GDPR, CCPA), and proper data deletion policies.

D. User Support & Dispute Resolution

If a user notices an error in their credit report or alerts, the process for disputing, resolving, or appealing must be clear and supported. As a relatively new app, the maturity of its support infrastructure may be under development.

Delays or weak support for critical issues (e.g. identity theft) could damage trust.

E. Competition & Market Penetration Risk

CreditVana is entering a competitive space, with established players like Credit Karma, NerdWallet, WalletHub, etc. Users may hesitate to trust a new entrant without long track record.

Convincing users to migrate or adopt a new app requires standout value (accuracy, cost, reliability) and strong marketing.

F. Regulatory & Compliance Risk

Credit reporting is heavily regulated. Missteps in compliance (data sharing, privacy laws, credit dispute protocols) can lead to fines or regulatory action. As CreditVana grows across jurisdictions, ensuring regulatory compliance at scale is challenging.

6. Comparison With Competitors

Understanding how CreditVana stacks up relative to alternative apps helps clarify its strengths and positioning.

A. CreditVana vs Credit Karma / NerdWallet / WalletHub

- Coverage: Some legacy apps cover only one or two credit bureaus, whereas CreditVana claims full three-bureau coverage.

- Free model: CreditVana emphasizes truly free score access, avoiding trial-conversion strategies; competitors often rely on upsells or premium features. CreditVana review

- Alerts & monitoring: Many competitors offer alerts; CreditVana competes by promising speed, clarity, and interface simplicity.

- Product offers: All offer affiliate products; success depends on relevance and user alignment.

B. CreditVana vs Traditional Credit Bureaus / Paid Services

- Bureaus like Experian, TransUnion typically require paid access or limited free report frequency; CreditVana offers easier, mobile-native access.

- Paid services (e.g. myFICO) offer deeper detail, forecasting tools, etc. CreditVana is less deep (for now) but more accessible.

C. Strengths & Moats

- If CreditVana consistently delivers accurate three-bureau data with responsive alerts and a clean UX, that can be a differentiator.

- Its affiliate marketplace is a potential monetization moat — users stay in-app to explore offers tailored to their credit profile.

- However, to maintain competitive advantage, it must keep improving features, security, and trust.

7. SEO, Branding & Marketing Suggestions

Given your aim for high visibility and user adoption, here are suggestions from an SEO / content / branding perspective.

A. Content Strategy & Thought Leadership

- Publish in-depth guides: “How to read a credit report,” “Ways to raise your credit score step by step,” “CreditVana vs Credit Karma comparison,” etc.

- Use case studies / user stories: real users who improved their score via CreditVana.

- Create video or infographic content explaining credit components, alert mechanisms, and app walkthroughs.

- Maintain a blog with frequent content updates — helps with fresh SEO signals.

B. On-Page & Technical SEO

- Each blog post and landing page should include target keywords (e.g. “CreditVana review,” “free credit score app,” “CreditVana vs …”)

- Optimize meta titles, meta descriptions, H1/H2 tags, alt text, internal linking, and schema markup (especially for “SoftwareApplication”).

- Ensure mobile friendliness, fast page load, secure HTTPS, and clean site structure. creditvana review.

C. Backlink Strategy & PR

- Partner with personal finance bloggers, credit education websites, fintech news sites to host reviews, guest posts, or coverage.

- Release announcements for new feature launches, expansions or security audits to attract press attention.

- Engage influencers in finance or fintech niches to review the app, boosting user trust and backlinks.

D. Trust Signals & Social Proof

- Show “As seen in” logos for media where CreditVana is featured (e.g. BIIA, tech news).

- Include user reviews, ratings, and testimonials (with names/pseudonyms) on homepage.

- Publish metrics: number of users, credit checks run, alerts delivered (if safe to share).

- Publish security credentials, data privacy certifications, or audit reports.

E. Keyword Focus & Long-Tail Strategy

- Use “CreditVana review” as the primary keyword (in title, intro, alt tags).

- Target long-tail variants: “CreditVana free credit score app 2025,” “CreditVana vs Credit Karma,” “is CreditVana legit review,” “CreditVana features and pricing,” etc.

- Use semantic keywords: “credit monitoring,” “credit report alerts,” “credit score tracking,” etc.

8. Final Verdict & Recommendations

Strengths Summary

- Truly free core offering: Access to credit score without trial traps is a major attractor.

- Three-bureau coverage: If delivered accurately, this is a strong selling point.

- Polished UI & mobile experience: Early user reviews applaud simplicity and clarity.

- Alerts & monitoring built-in: A must-have in credit apps and done cleanly here.

- Marketplace of financial products: Provides monetization and utility.

Key Weaknesses / Risks

- Premium feature upsells or hidden limitations may frustrate users.

- Some transparency gaps in terms, cash advances, support, and feature limitations.

- Trust & accreditation are still in development (e.g. BBB not accredited).

- Data / security risk inherent in credit apps; must maintain strong safeguards.

- Competitive pressure from entrenched incumbents in the credit space.

Recommendation

For users who want free, user-friendly access to their credit score, CreditVana review is a strong proposition worth trying. Its core features (score, alerts, credit report card) are compelling, especially given the positive reviews and clear UI.

However:

- Proceed with caution if relying on premium or advance features — read terms carefully.

- Double-check your credit report via bureau sites if you notice discrepancies.

- Avoid committing to paid upgrades until you’re confident in the app’s value and support.

For the company / brand side, to scale and build trust, I recommend focusing on:

- Full transparency around fees, limitations, and premium tiers

- Independent security audits and publishing those results

- Expanding user support & dispute resolution infrastructure

- Aggressive content & PR campaign to solidify authority in credit space

- Show third-party verification or accreditation (e.g. financial regulators, trust seals)

if tou want to read other articles about creditvana review read now